Originally Published on Bloomberg Law, April 14, 2026, 4:30 AM EDT

The Department of Justice’s declination of charges against French medical device company Balt SAS and its US subsidiary Balt USA LLC is more than a compliance case study. It is a roadmap for how anti-corruption risk should be assessed, allocated, and addressed in medical device M&A.

The Balt matter, which involved bribes paid to a doctor employed by a French-state-owned public hospital through a Belgian consultant, generated revenue of approximately $1.68 million for Balt and roughly $1.21 million in profit. DOJ declined prosecution after Balt self-disclosed, cooperated, and disgorged the profit, while French authorities imposed penalties of €1.77 million and compliance obligations. Balt SAS’s swift self-disclosure or autorévélation after uncovering the scheme led to this favorable outcome, but the six-year duration of the bribery reveals gaps in its M&A diligence and post-acquisition anti-corruption compliance controls at its newly acquired subsidiary.

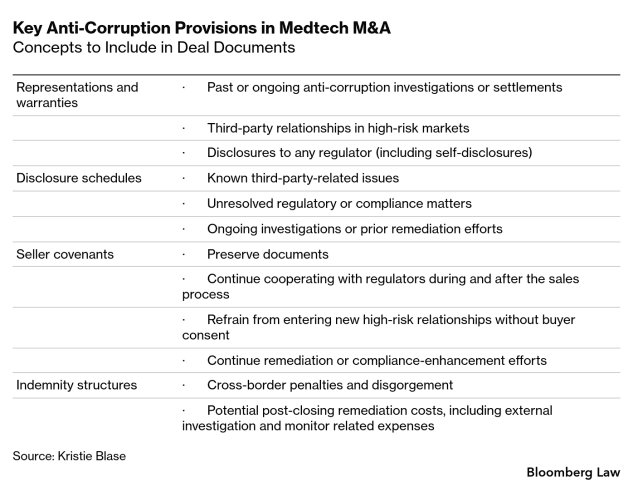

For acquirors, sellers, brokers, and counsel, the takeaways are clear: Medtech deal diligence must be designed to surface anti-corruption exposure across jurisdictions to incorporate that risk into deal structure and economics. Integration must then prevent Balt-style schemes from emerging post-close—when earnouts are done but liability risk is not.

High Risk Globally

Medical device companies are potentially exposed wherever they interact with state-owned or privately-owned hospitals, public-health systems, or government-affiliated healthcare professionals. Consultants, distributors, and regional agents are often the primary channel for kickbacks. The Balt scheme is a classic red-flag pattern that often appears in enforcement actions: sham consulting agreements, double-invoicing, and payments routed through intermediaries.

From an M&A perspective, medtech deals mean that diligence requires extra attention to distributor and consultant relationships, as these can trigger bribery, Foreign Corrupt Practices Act, and local law exposure even in countries that aren’t generally thought of as high-risk for corruption. Buyers (and sellers) should expect that transactions in this space are high risk and will attract scrutiny from multiple regulators.

Valuation and Deal Structure

In practice, the Balt resolution is likely to affect not only diligence scope but deal economics. Where a target has used third-party consultants or distributors in higher-risk markets, buyers may respond by reducing upfront consideration, expanding escrow, and requiring a special indemnity for pre-closing anti-corruption exposure. That shift is particularly important in medtech, where earnouts and deferred consideration are already typical features and buyers may respond by keeping a larger portion of seller value at risk until the buyer has confidence that the target’s compliance controls can support the business after closing.

From a buyer’s perspective, Balt-style anti-corruption risk is usually priced as a mix of liability, timing, and execution risk. Where diligence shows a bounded historical issue, the buyer may still proceed, but it will often shift more value out of the upfront price and into an escrow, holdback, or earnout so that the seller remains exposed if remediation costs or regulator scrutiny are worse than expected.

In pharma-adjacent deals, cases such as Teva Pharmaceuticals ($519 million FCPA resolution for bribes in Russia, Ukraine, and Mexico to secure regulatory and formulary access) and Alexion ($21 million to resolve FCPA charges for payments to favor Soliris prescriptions) illustrate how such risks distort revenue quality, justifying valuation discounts or heavier contingent payments. Buyers price both probability and duration: A messy third-party footprint creates a wider valuation gap because of the time and uncertainty in unwinding it.

The US-French Lesson

From 2017 to 2023, Balt used a third-party consultant to pay $600,000 in bribes to a French doctor for using Balt devices, disguising the payments as consulting fees and bonuses. The scheme was carried out by the former owners and founders of Blockade Medical, which was acquired by Balt SAS in 2016 and subsequently operated as Balt USA LLC. The bribes—by way of fake invoices, fake “training courses,” and “bonuses”—were not discovered until six years after the deal closed.

The Balt resolution demonstrates that US and French authorities are coordinating on facts, timing, and penalty structures. DOJ credited Balt’s voluntary self-disclosure, cooperation, and remediation, while the French PNF resolution included compliance obligations that DOJ declined to duplicate. The UK Serious Fraud Office and Financial Conduct Authority similarly expect and reward voluntary self-reporting, particularly by life sciences companies that are vulnerable to distributor- and consultant-related enforcement. For M&A, this means buyers should treat anti-corruption risk management as a core part of deal economics, not a back-office compliance issue.

Practical Takeaways

The cross-border Balt resolutions offer important lessons for deal structuring and execution.

The timing of self-disclosure can have a material effect on a deal. Both DOJ and PNF emphasized the early disclosure—before the company’s internal investigation was complete—as a principal reason for leniency. If an anti-corruption issue first surfaces during deal diligence, the parties should treat the disclosure as both a regulatory and transactional inflection point: Prompt self-disclosure may improve the enforcement outcome, but it may also delay signing, complicate financing and RWI placement, or kill the transaction entirely.

Coordinating with US and foreign authorities can create real deal value by reducing duplicative penalties, limiting or avoiding overlapping remediation demands, accelerating closure of parallel investigations, and improving certainty around timing, closing, and post-closing exposure.

For a seller, remediation and documented compliance improvements should be part of deal preparation. Sellers that can present a credible anti-bribery compliance narrative at the outset of the deal process are better positioned to defend valuation, narrow indemnity demands, and limit pressures for larger escrows or contingent consideration.

From a buyer’s perspective, diligence should focus on whether the target has a centralized third-party risk register, a track record of self-disclosure or regulatory resolution, and a documented process for coordinating regulators across jurisdictions. Those points tell the buyer whether the risk is contained, recurring, or likely to create cross-border follow-on exposure.

Post-closing integration and compliance program monitoring matter for both sides. Balt illustrates why: The scheme began after the company was acquired, showing how integration failures can create compliance risk long after earnouts are settled. For sellers, performance determines earnout achievement and escrow release. For buyers, it’s the time to resolve diligence findings, integrate compliance controls and culture, and terminate problematic third-party arrangements.

Deal Terms

The more a diligence review uncovers unknown or poorly documented third-party relationships, the less likely ordinary reps and warranties alone will solve the problem. Sellers should expect buyers to ask for a longer survival period for compliance representations, a narrower cap on excluded claims, and covenants requiring document preservation, regulator cooperation, and continued remediation through closing. The more opaque the third-party footprint, the more leverage the buyer has to demand a special indemnity, tighter disclosure schedules, and a longer survival period for anti-corruption reps.

If the target can’t document the consultant or distributor relationships cleanly, the buyer is likely underwriting the risk as a live liability rather than a legacy issue, which almost always means a lower valuation or a heavier contingent-payment structure.

In the medical-device market, legacy issues like those at Medtronic ($9.2 million kickback settlement involving physician payments and device sales) give buyers leverage to expand escrows (10-15% of enterprise value) and tie earnouts to clean post-close milestones.

Practical Diligence

The deal diligence workflow should be built around the risk profile of the target company.

Key pieces should include:

Third parties. Identify high-risk distributors, consultants, and agents; review contracts, commission structures, and prior audits.

Health-care professionals. Identify and carefully review consulting, speaker, and key opinion leader (KOL) arrangements, including payment records, travel-related expenses, and transparency reporting filings.

Payment controls. Test whether approvals, invoices, and M&A-related systems can detect or prevent sham payments or double-invoicing.

Training and culture. Confirm that anti-corruption training reaches sales, commercial, and local management in key medical device markets, and that whistleblowing reporting channels are functional.

Anti-corruption issues in the medical device space don’t end at signing or closing. From escrows and earnouts to post-closing cooperation with regulators, the Balt matter shows that deal lawyers should treat compliance risk as a continuing integration issue, not a one-time diligence exercise. The Balt conduct began after the company was acquired—likely years after any earnouts settled—underscoring how post-closing commercial pressure can create compliance risk if controls don’t keep pace with growth expectations.

This article does not necessarily reflect the opinion of Bloomberg Industry Group, Inc., the publisher of Bloomberg Law, Bloomberg Tax, and Bloomberg Government, or its owners.

Author Information

Kristie Blase is a partner at Frazer + Blase, guiding mid-market/tech companies through capital raises and M&A.

Copyright 2026 Bloomberg Industry Group, Inc. (800-372-1033) www.bloombergindustry.com. Reproduced with permission. Cover Illustration: Jonathan Hurtarte/Bloomberg Tax.

" height="39.101000457763675px" id="v3jGvdhkA" transform="translate(0 0.5)" width="471.9989968261719px"/><path d="M 273.539 23.743 L 273.56 23.743 C 284.594 23.743 286.632 15.955 286.632 11.698 C 286.632 5.394 281.581 0.455 272.585 0.455 L 255.027 0.455 L 255.135 23.721 Z M 272.076 4.972 C 277.777 4.972 281.039 8.243 281.039 12.37 C 281.039 16.497 277.842 19.118 272.141 19.118 L 260.684 19.118 L 260.619 4.972 Z M 18.512 23.743 L 18.534 23.743 C 29.567 23.743 31.604 15.955 31.604 11.698 C 31.605 5.394 26.555 0.455 17.559 0.455 L 0 0.455 L 0.108 23.721 Z M 17.049 4.972 C 22.749 4.972 26.012 8.243 26.012 12.37 C 26.012 16.497 22.815 19.118 17.114 19.118 L 5.658 19.118 L 5.593 4.972 Z M 300.669 34.704 L 300.669 27.003 L 295.076 27.003 L 295.076 39.556 L 321.847 39.556 L 321.847 34.704 Z M 295.076 0.455 L 295.076 23.743 L 300.669 23.743 L 300.669 0.455 Z M 398.972 23.72 C 393.856 15.965 376.688 19.085 376.688 10.961 C 376.688 7.539 379.528 4.755 386.182 4.755 C 389.651 4.755 393.498 5.762 396.923 7.939 L 398.766 3.466 C 395.514 1.235 390.767 0 386.182 0 C 375.897 0 371.204 5.145 371.204 11.178 C 371.204 21.154 382.378 21.435 389.38 23.721 C 389.401 23.731 389.434 23.742 389.455 23.742 L 398.972 23.742 M 435.854 34.704 L 435.854 39.556 L 407.458 39.556 L 407.458 23.624 L 413.05 23.623 L 413.05 34.703 L 435.854 34.703 Z" fill="rgb(37, 75, 117)" height="39.55600025939941px" id="MEnZDRgPJ" transform="translate(36 0)" width="435.8540078125px"/><path d="M 26.771 10.961 L 26.771 15.813 L 0 15.813 L 0 0 L 5.593 0 L 5.593 10.96 L 26.771 10.96 Z M 99.203 3.107 C 99.203 3.107 99.268 3.205 99.29 3.259 L 99.279 3.259 C 99.279 3.259 99.235 3.151 99.203 3.107 Z" fill="rgb(37, 75, 117)" height="15.812999999999999px" id="FE_6wC8sG" transform="translate(331 23.5)" width="99.29000292968749px"/><path d="M 400.305 7.407 C 400.305 13.387 395.504 18.52 385.153 18.52 C 379.181 18.52 373.307 16.517 370.175 13.603 L 372.245 9.249 C 375.149 11.87 380.124 13.766 385.153 13.766 C 391.927 13.766 394.832 11.144 394.832 7.743 C 394.832 7.592 394.821 7.451 394.81 7.31 C 394.81 7.245 394.81 7.17 394.788 7.104 C 394.767 6.85 394.717 6.599 394.637 6.357 C 394.616 6.28 394.591 6.203 394.561 6.129 C 394.552 6.1 394.541 6.071 394.528 6.043 C 394.497 5.954 394.461 5.868 394.42 5.783 C 394.387 5.696 393.639 4.006 389.379 2.263 L 398.896 2.241 C 399.914 3.931 400.197 5.772 400.208 5.901 C 400.229 6.075 400.251 6.259 400.262 6.454 C 400.273 6.552 400.283 6.649 400.283 6.747 C 400.283 6.963 400.305 7.18 400.305 7.407 Z M 367.91 18.076 L 362.046 18.076 L 355.272 2.241 L 360.713 2.241 Z M 339.599 2.24 L 332.619 18.076 L 326.875 18.076 L 334.039 2.263 L 339.599 2.241 Z M 172.516 1.548 L 181.273 18.065 L 187.364 18.065 L 177.729 0 C 175.8 0.996 172.516 1.549 172.516 1.549 Z M 0 18.076 L 5.593 18.076 L 5.593 2.263 L 0.033 2.241 Z" fill="rgb(37, 75, 117)" height="18.51999993705749px" id="lrM07ntHs" transform="translate(36 21.5)" width="400.30498779296875px"/><path d="M 209.778 23.288 L 209.799 23.288 C 220.833 23.288 222.87 15.5 222.87 11.243 C 222.87 4.939 217.82 0 208.824 0 L 191.266 0 L 191.374 23.266 Z M 208.314 4.517 C 214.015 4.517 217.278 7.788 217.278 11.915 C 217.278 16.042 214.08 18.663 208.379 18.663 L 196.923 18.663 L 196.858 4.517 Z M 191.342 39.101 L 196.934 39.101 L 196.934 23.288 L 191.374 23.266 Z M 5.593 23.287 L 0 23.287 L 0 39.101 L 5.593 39.101 Z M 161.535 23.168 L 155.942 23.168 L 155.942 39.101 L 184.338 39.101 L 184.338 34.249 L 161.535 34.249 Z M 150.025 34.249 L 150.025 39.101 L 117.326 39.101 L 117.326 35.3 L 126.864 23.492 L 133.497 23.525 L 124.815 34.249 Z M 84.734 23.288 L 77.754 39.101 L 72.02 39.101 L 79.184 23.288 Z M 113.043 39.101 L 107.18 39.101 L 100.417 23.287 L 105.857 23.287 Z M 370.271 23.266 L 375.82 23.266 L 375.809 23.288 L 370.26 23.288 Z" fill="rgb(37, 75, 117)" height="39.10100074768066px" id="ax4U1_tVb" transform="translate(0 0.5)" width="375.820009765625px"/><path d="M 24.322 0 L 3.067 0 L 0 4.863 L 21.254 4.863 Z" fill="rgb(37, 75, 117)" height="4.8629999999999995px" id="hBMZZnDrT" transform="translate(120.5 19)" width="24.322000000000003px"/></g></svg>)